Ad Networks 2.0 are dead. Long live Ad Networks 3.0.

Curation is nature healing

Welcome back to GHAT! I’m excited to bring you the latest edition, because I spend more time thinking about ad tech than I should, and it will give me a bit of catharsis if I can subject all of you to my ad tech curse even if just for a few minutes.

Today I’d like to reframe things. I think ad tech has done that good old ad tech thing where shit has gotten super confusing again. People are talking about Curators, Signal, Agents, you name it – like we’ve invented a bunch of new things.

We haven’t.

We’ve just made up names for the same things happening in different places. Don’t get me wrong, the same thing happening in new places can drastically change the landscape of an ecosystem – but it can also serve to confuse and befuddle, when in reality, I am of the opinion that ad tech is healing itself and becoming simpler.

I will tease all of you with my shower thought that spurred the rest of this article, and it was a silly “omg this is true” moment for me. That thought is that I am fairly certain, with a bit of shoe-horning and an army of ops people (or agents perchance?), I could recreate the entirety of Ad Tech in Google Ad Manager (GAM).

All of it.

Creative trafficking, placement level targeting and optimization, data. You name it. I could do all of it in GAM. I’m just gonna need to export a lot of ad tags and upload a lot of line items. This is because fundamentally, all of ad tech consists of a few basic functions. Sure we’ve built a bunch of companies, and we’ve invented the ridiculous concept of “buy side” and “sell side” ad tech, and we’ve modularized the components of the system – but at its core, what OpenRTB, and what all of independent ad tech seeks to do is create a simple marketplace of supply and demand, targeting the demand to the supply. Because of this, with sufficient will, we could absolutely execute that vision within a single GAM account. It’s a wild thought. And it should scare you, because it’s indicative of the unnecessary complexity that we’ve introduced through all of our ad tech shenanigans.

With this logic in mind, I’d like to reframe the emergence of Curation. I love Ciaran and Kev’s “SSA (super signal aggregator),” framework, and their investment thesis around signal, but I think it overcomplicates things. Signals have always existed in ad tech, every component of a bid request is a signal, and data signal vendor aggregators are actually nothing new (in fact, this was the original job of the DSP). I actually think focusing on signal, as opposed to function, makes the landscape look confusing. Curation begins to make a lot more sense if you do a feature comparison of each of the companies in the value chain, and we plot those over time. So that’s what we’re going to do!

Let’s start here – pre-curation and pre-header bidding life :

I don’t expect this image to be exhaustive, sure there are probably a few features and functions in there that I missed, but this is the core of it. This was a simple world where DSPs ran campaigns, and SSPs executed their most important function – “Buyer Auction Hosting”. In this scenario, the SSPs are the holders of auctions. There are other auctions to be sure – the internal DSP auction, the ad server auction, but those auctions are not aggregating prices across many DSPs for a given impression. The SSP auction is the programmatic auction in this era.

And SSPs were closed systems, which actually really sucked. In your core adserver, because nobody was bidding, you had to traffic an estimated yield per SSP, which of course would vary wildly based on how many exchanges were called before them, and I feel quite comfortable saying that this era, while discrete and easy to understand (DSPs = Buyers, SSPs = Marketplaces), the publishers got totally screwed..

The reason is simple – the closed nature of SSPs meant that demand was wildly fragmented. That fragmentation meant that inter-SSP competition was really almost non-existent, and publishers actually had zero clue on an impression by impression basis what each impression was actually worth – and rarely were there other bidders to push the price up. So things sold cheap in auctions with relatively few participants – especially compared with a modern header bidding auction! Imagine, a single SSP, vs a header bidding auction with 30 exchanges calling 200 DSPs each – the bidder density difference is easily an order of magnitude.

So yea, this era, while simple, sucked.

But then, we invented header bidding

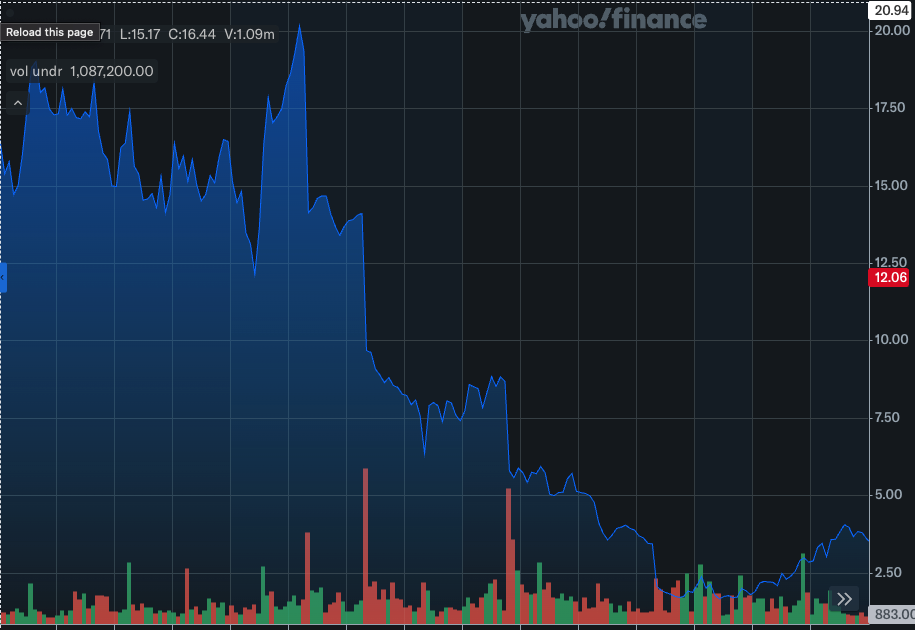

Header bidding, at its core, created a second auction outside of the one that occurred inside of the SSP. At first some SSPs resisted, because the fragmentation that drove their margins and market positions was directly threatened by HB (especially if you were early in the stack). But HB won. HB really won. Look how much it won here :

That, my friends, is Rubicon’s stock price between 2015 and 2018. And that’s the visualization of someone betting against header bidding, which is the embodiment of a competitive market as opposed to a fragmented one. This is because 3 b-grade SSPs participating in a competitive auction mops the floor with a single a-grade SSP in a fragmented implementation.

But I digress. The actual thing I’d like to illustrate in my first diagram is that the most important function of an SSP (in my opinion), the Buyer Auction Hosting, is now shared. Two things are doing it. There’s a SSP buyer auction, and there’s a Prebid buyer auction.

That’s redundant. It was redundant in 2016, it’s redundant in 2025. We simply don’t need two systems to manage auctions with bidding systems.

The obvious upshot of this is that the bidders who traditionally bid into the SSP auctions can now leap-frog the SSPs and bid directly into the prebid auction. I swore until I was blue in the face running RTK that this would happen and happen fast.

But it didn’t.

There are probably 5x the number of Prebid bidders that there are DSPs – what we saw is that DSPs had drunk their own kool-aid of being buy-side people, and had somehow convinced themselves that bidding into prebid was a “sell side function,” even though it was literally technologically identical. Oh, that and the fact that we came to learn that tons of Agency Holding companies have deals in place with ad exchanges, where they can extract margin at the ad exchange level and engage in shenanigans, but this isn’t a missive about corruption.

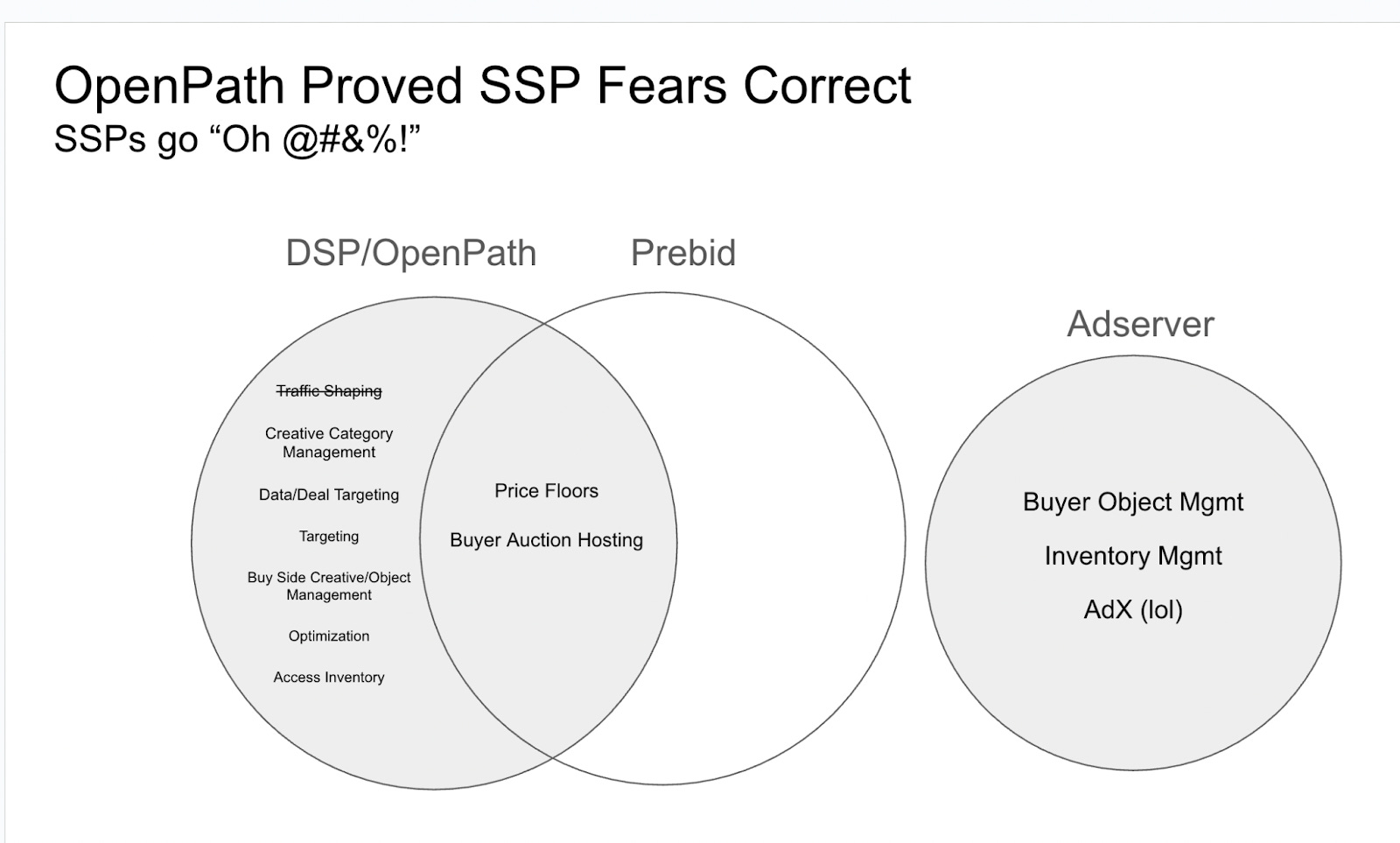

What we did see is one enterprising DSP figure this out and begin to get involved with Prebid – The Trade Desk. I remain gobsmacked that more DSPs have not gotten in on the game – but I guess I’ve heard about a few internationally. But let’s visualize TTD’s OpenPath :

Zoinks. As you can see, the redundancy (the features shared in the Venn diagram) that came about as a result of header bidding created an opportunity for disintermediation.

This makes perfect sense.

The universe hates inefficiency. It took us 10 years, but eventually this redundancy was laid bare – and it resulted in the worst case scenario for SSPs, which is one of their primary revenue sources cutting them out of the equation.

I don’t think anyone was actually surprised by this. The moment prebid emerged anyone with a brain knew “wait, if there’s another auction, why don’t DSPs just bid into that?” – It just took the DSPs awhile to pull their heads out of their keisters and get the work done. But to be honest…most DSPs still haven’t done it. And the same way that Prebid took off like a rocket as a way for SSPs to equal the playing field with Google, those wily exchanges figured out a way to prevent this DSP disintermediation.

That way is curation.

The crux of this article is that Curation is simply SSPs playing defense. Prebid was the first domino to fall, moving SSP functionality out of the SSP and making them redundant. SSPs were now resigned to slowly watching their businesses dwindle as more and more innovation happened in the primary buyer auction, the Prebid auction.

But in their infinite wisdom, they realized “If Prebid can take functionality away from us, what if we could take functionality away from the DSPs?”

Getting people to change DSPs is impossible. Everyone knows that. Ask Chango. But Prebid’s appeal was that it didn’t replace SSPs, it wasn’t an alternative, it just took one or two things that they did and moved them while still cooperating with them. In fact, it benefited them and they are the ones who designed it!

So, if I’m an SSP, I’m wondering what parts of a DSP could I move out of the DSP, thereby entrenching myself in the value chain?

Well, turns out most. And it turns out that most DSP functions actually work better when you’re close to the inventory. This is because Header Bidding created a glut of duplication and noise, and DSPs haven’t done what they need to do to make things work better (ie. pick 2 exchanges, ditch the rest). My thesis on this one is that they became addicted to buying UserID lists, and that’s an easy business to run, so they didn’t think to invest in actually optimizing what they were buying. As long as they “got their ID,” it was gucci. So they’re now sleeping in a bed that they’ve made.

So what does this functionality shift look like?

We now see the Venn diagram creeping the other direction. SSPs, through deal ID infrastructure that they’d built ages ago, actually already had the skeleton of targeting systems – all they needed to do was a little bit of workflow work to turn this into a UI a media buyer could use to change what inventory went to campaigns. And because SSPs were so close to the inventory, and inherently didn’t have the ridiculous duplication that all DSPs can’t seem to convince themselves to turn off, campaign optimization works better in the SSP than in the DSP.

And that brings us to the current day. One thing I’d like to emphasize is that this trajectory hasn’t actually created any new functionality. What it has done is moved features and functions from one class of company to another – which brings me to what I think is the important conclusion of this article

Buy Side and Sell Side frameworks for viewing the industry are outdated.

There are Bidder Networks and there’s Prebid. That’s it. Prebid is the monetization auction, and the Bidder Networks are the bidding mechanisms. Maybe they’re DSPs – maybe they’re DSPs + SSPs + Curators – but at the end of the day, the output of those systems is a bid, and the functionality within them is identical in that their simple goal is to derive a bid and spend budgets.

This is a good thing.

The concept of buy side and sell side holds us back when competing with walled gardens – it puts two hands into the cookie jar when walled gardens only have one, not to mention the data asymmetry and inefficiency that comes from integrating two ancient ad tech companies. Andthe Google ruling means that things are going to get even more egalitarian if AdX has to bid into prebid, at which point we’ll finally get pretty close to recreating walled garden performance (yes, the final hurdle for the open internet is the artificial insertion of GAM into the monetization flow).

But the world is indisputably getting simpler and therefore better. We now have bidders, in a few different flavors, and we have Prebid. Soon, we might even be free of GAM. And just in time for LLMs to destroy the internet as we know it, we might actually build systems that rival Google and Facebook.